Ireland's public debt increased by €5 billion last year.

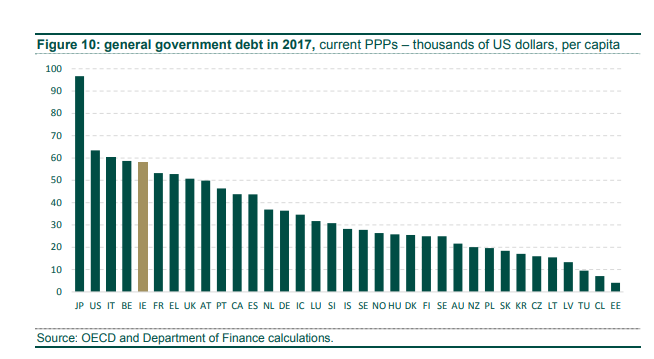

The annual report on public debt shows it rose to €206 billion in 2018 - the equivalent of €42,500 for every person living in the State.

It's among the highest 'per capita' debt rates in the OECD.

The Department of Finance says fiscal discipline must be shown to stop the build up of any more debt.

It says structural reforms - such as raising the level of employment and reducing barriers to the labour supply - will be important in reducing the debt burden.

They also say the annual interest bill is a "significant operating cost" for the State, sitting at €5.2 billion in 2018.

Explaining the main €206 billion figure, Finance Minister Paschal Donohoe said: "[It's] obviously a very big figure.

"The important thing from our point of view is that there are positive trends afoot - regarding how it's decreasing as a percentage of everything we make and sell in our country.

"We just need to be careful about this in the future, and be careful about getting it down to a lower level."

He explained that recent years have seen the country running deficits, meaning the Government needed to borrow to fund day-to-day spending.

However, he noted: "We're now in a place where we're going to be running surpluses. The really important thing is to continue to run them, because that will reduce our debt and help make the economy safer."